Concreit’s Next-Gen Financial Wellness Study

Published on

July 28, 2019

Interested in growing wealth through investing in rental homes? Join the Priority Access List today.

With each generation holding their own distinct set of views, beliefs, and habits formed as a result of the specific societal and economic backdrops that they come of age in, marketers and brands attempt to decode these cohorts in order to tailor businesses and strategies that will resonate with them.

The financial services industry is no different. Facing an inflection point, where the consumerization of IT is increasingly democratizing the way people manage their financial lives, and technologies like blockchain and cryptocurrencies are beginning to look more and more like disrupting forces, organizations are more incentivized than ever to understand the financial lives of these younger generations.

With Generation Z already on track to become the largest generation of consumers by the year 2020, and millennials inching toward their peak earning years, the inability to service the financial needs of these generations is simply not an option.

The team at Concreit wanted to get a current pulse on just how Gen Z and millennials feel about their finances today, and what they are or aren't doing, to ensure long-term financial wellness. To do so, we commissioned a research study to 1,000 Americans, nearly evenly split between Gen Z (18-23) and millennials (24-38).

Here’s what we found:

Millennials Turn Attention to Making Ends Meet, While Gen Z Still has FOMO

When asked “What currently takes priority in terms of your savings?” building an emergency fund was the number one response for millennials, ahead of a down payment for a home (19%) and travel (16%). Interestingly, retirement and student loans tied for last place at 14%.

Somewhat unsurprisingly, Gen Z’s number one priority is paying for their education/student loans, with 38% saying that takes precedent. Saving for travel came in second, followed by building an emergency fund. The same percentage of Gen Z & millennials reported that they are not currently saving (13%).

While these differences in priorities may be attributed in large part to the specific life stage that each generation is in, the differences we found between these two generation’s top financial concerns may signal more fundamental differences in how they think about money.

When asked, “What is your biggest financial concern?” millennials say that “Not being able to pay my bills” is their top worry (26%), followed by “Not being able to live the lifestyle I’d like to” (25%) and “Not being able to retire when I’d like to” (21%). Whether it’s the crushing cost of living in major urban centers or a broader shift in the American dream, not being able to save enough for a down payment for a home (16%) was even further down millennials’ concern list.

What was Gen Z’s top financial concern? “Not being able to live the lifestyle I'd like to," with 38% choosing that as their top worry. Not being able to pay their bills came in second (25%) and not being able to pay student loans came in third (18%).

With the enormous amount of student loan debt saddling millennials, it’s notable that “Not being able to pay off my student loans” came in last for them and third for Gen Z. However, it could also be that as millennials age, their heightened concern for paying their bills and maintaining their lifestyle is a direct result of things like student loan debt which continues to siphon money from other goals like stashing money for retirement.

Young Americans are Using DIY Financial Tech More, but Trust in Robo Solutions Still in its Infancy

There are few more difficult life decisions to make than those pertaining to one’s finances. With the consequences of bad decisions causing significant setbacks and hardships, it’s no wonder that financial advice has become such a gigantic industry.

However, with many institutions still missing the mark when it comes to servicing these generations, and millennials and Gen Z showing a preference for making decisions on screens and communicating via platforms rather than on the phone or in person, one might assume a shared preference for a self-service approach when it comes to making money decisions.

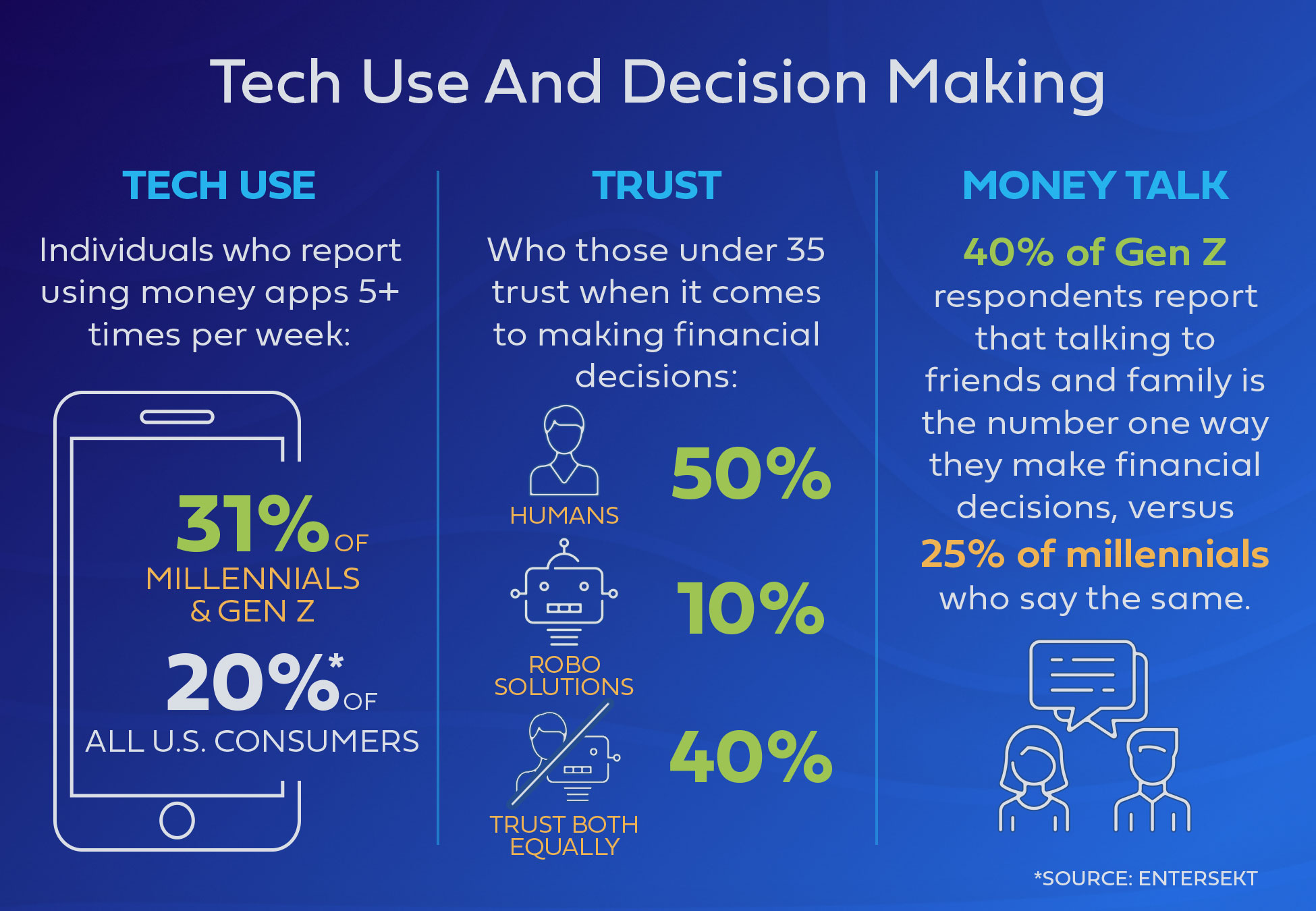

It’s true that both of these cohorts are comfortable using tech when it comes to their finances. Nearly one-third of Millennials and Gen Z (31%) report using banking, budgeting or investment apps daily five or more times per week. That’s compared with a recent survey that found 20% of all U.S. consumers use banking apps daily.

One would think that this proclivity for tech and the normalization of interacting with AI technology like digital assistants and chatbots might make these cohorts just as comfortable turning to robo solutions when it comes to making financial decisions. Well, not exactly. 51% of Gen Z and 48% of Millennials say they trust humans more than AI for making financial decisions. Gen Z takes this comfortability for talking with others about their finances to the next level, with 40% saying that talking to family and friends is the number one way they make financial decisions, versus 25% of Millennials who say the same thing. 58% of millennials reported that “Doing my own research” was the number one way they make financial decisions.

Only 16% of those under the age of 35 reported that “Working with a financial advisor” was the primary way they make financial decisions.

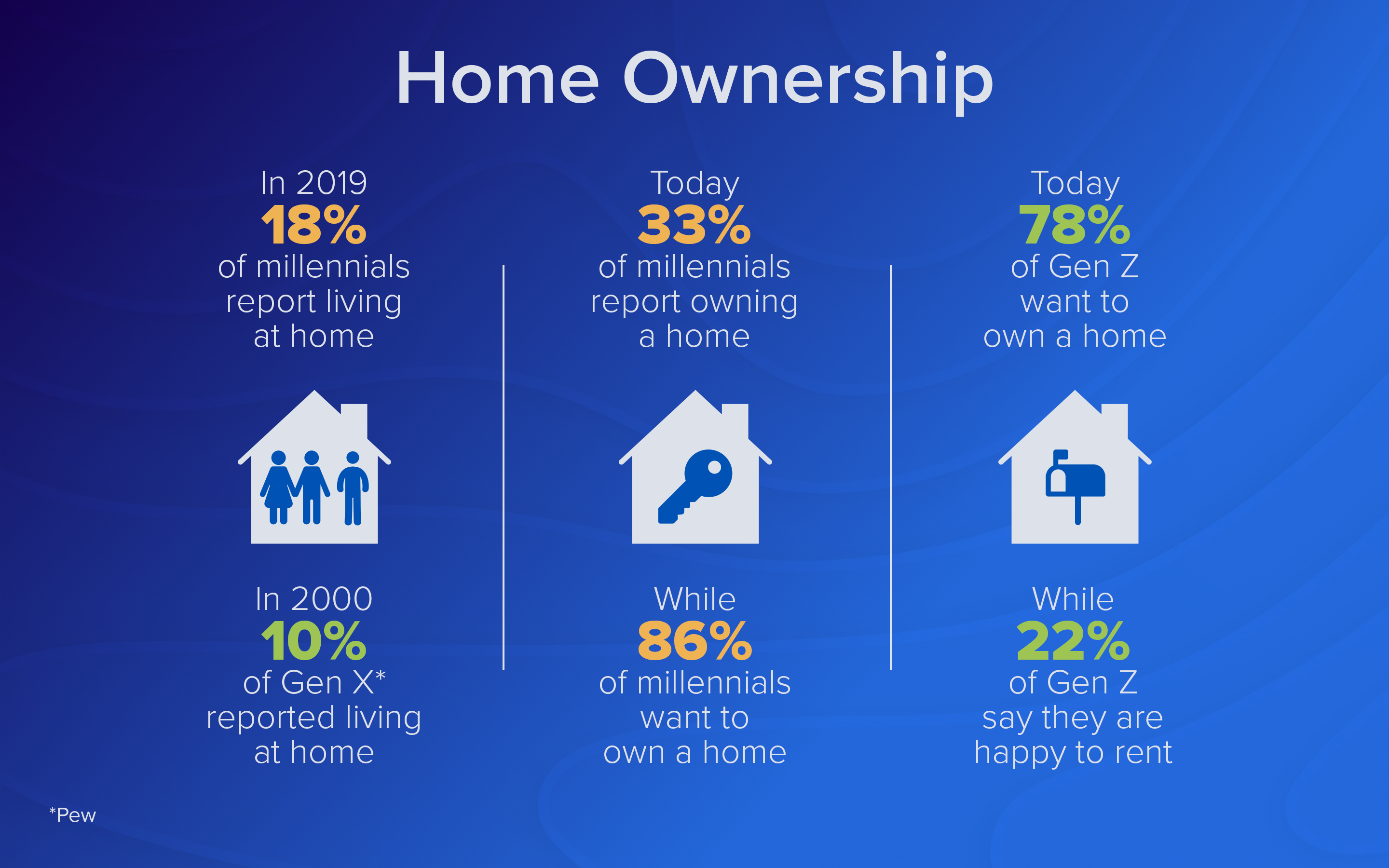

Nearly 1-in-5 Millennials Still Live at Home with Their Parents, Yet 86% Want to Own Their Own Home

With recent reports that nearly half of millennials receive financial assistance from their parents, it’s perhaps not surprising that our study found that nearly 1-in-5 (18%) of millennials are still living with their parents. That’s compared to 10% of Gen X that reported living at home in 2000 when they were the same age millennials are today.

We also found that 33% of millennials report currently owning a home, which is in line with U.S. Census Burea data. That’s 8 to 9% percentage points lower than previous generations’ homeownership rates within the same age. And it’s not for lack of wanting either. In fact, 86% of our millennial respondents reported that they want to own a home. Gen Z was slightly less likely to report the same (78%), and more likely (22%) to say that they are perfectly content with renting for the foreseeable future vs 15% of millenials who reported the same.

Other studies have shown that 70% of millennials said they are willing to cut back on extra-curricular activities, like shopping, movie-going and a spa visit, once a month to make home ownership happen. It will be interesting to see how Gen Z’s current focus on lifestyle and contentedness around renting evolves into a potential shift away from home ownership, one of the core pillars of the American Dream.

More than 1-in-3 of Those 38 and Under Expect to Retire by 60, But Millennials May Be Less Realistic

When it comes to financial wellness, retirement cannot be overlooked. With some experts saying that individuals should have 10 to 12 times their current income saved for retirement, the path to getting there can be a daunting one.

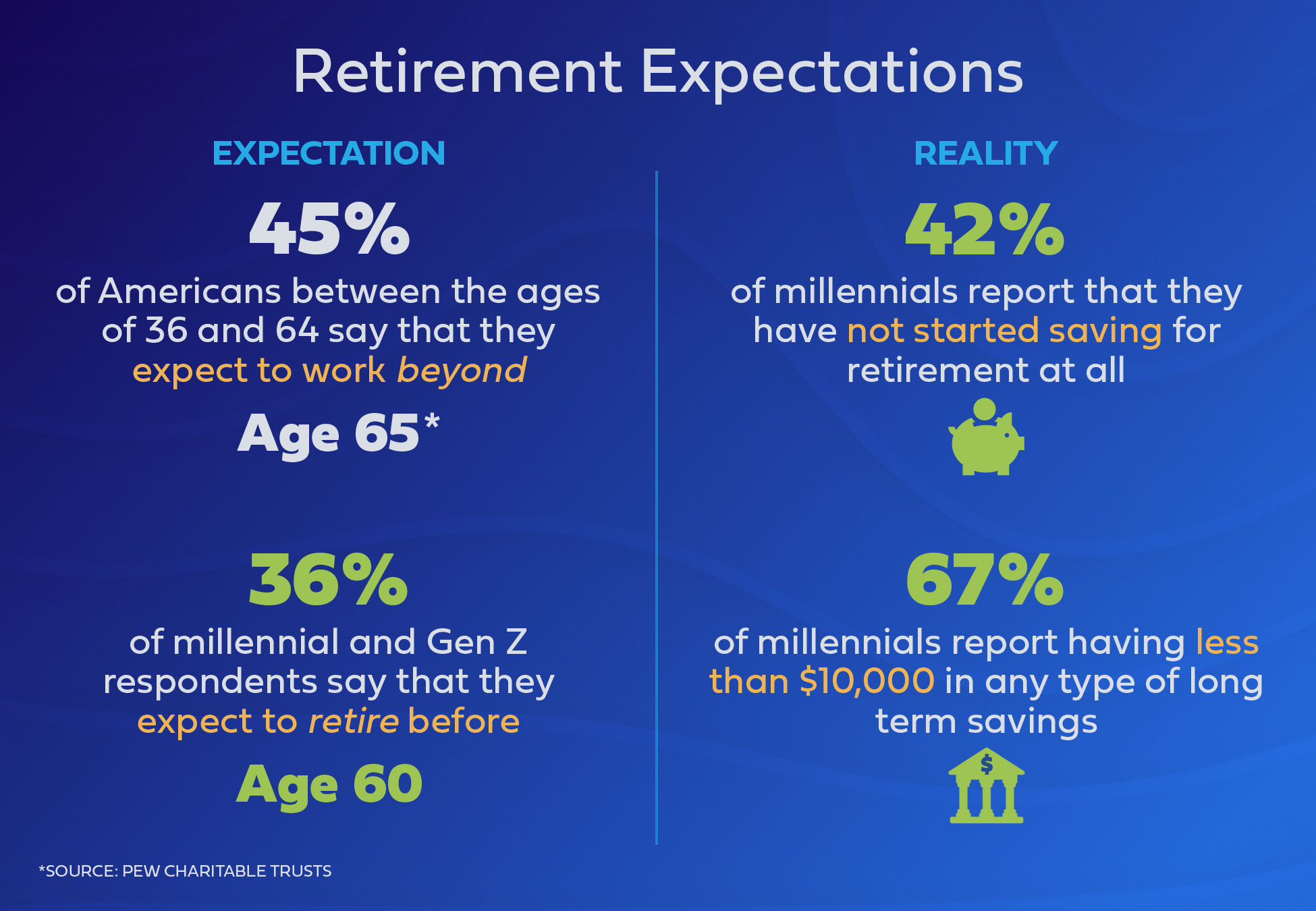

But like any journey, the path to retirement starts with setting expectations and goals. With a recent Pew study finding that 45% of Americans between the ages of 36- and 64-years-old say they definitely expect to have to work past 65, it’s interesting to note that more than one-in-three (36%) of our Gen Z and millennial respondents expect to retire before the age of 60.

While it may take some time to see where Gen Z nets out, as they’ve only recently entered the workforce, there appears to be a gap for millennials when it comes to expectations vs reality. One-in-three millennials expects to retire before or by 60, yet 42% of Millennials report that they have not started saving for retirement with a dedicated savings or investment account. On top of that, 67% report having $10,000 or less in any type of long term savings or investment account. With retirement experts like Fidelity suggesting that you should have twice your annual salary stashed away by age 40, it looks like many millennials may be forced to rethink their retirement plans.

Despite the fact that the oldest members of Gen Z have only been out of college for a couple of years, nearly one-in-three (32%) report they already have a dedicated savings or investment account for retirement -- a promising sign.

Number of Young Americans Investing in Stocks Continues to Decline As Confusion Abounds

With most experts agreeing that you can’t save your way to wealth, it’s important to make investing a part of your lifestyle as early as possible. So how do Gen Z and millennials stack up when it comes to leveraging the power of investing?

Let’s start with the stock market. A 2018 Gallup poll found that the percentage of people less than 35-years-old with money in the stock market in 2017 and 2018 stood at 37%, down from 52% for people in that age range in the two years (2006-07) leading up to the crash of 2008. Our study illustrates a continuing slide, with 35% of our Gen Z and millennial respondents reporting that they invest in stocks.

After stocks (mutual funds/ETFs etc.), the second most popular investment for millennials is real estate, with 13% saying they invest in some form (physical property, REITs, etc.), followed by cryptocurrency at 12%. Gen Z seems to have a slightly larger risk appetite, reporting that their second most popular (12%) investment is an alternative investment (cars, art, collectibles), and cryptocurrencies came in third (11%).

With 46% of Millennials saying they aren't investing whatsoever, and 57% of Gen Z reporting the same, we wanted to see how comfortable these generations feel about the idea of investing. After all, it’s widely agreed that there’s a pervasive state of financial illiteracy amongst the American youth.

We found that nearly the same amount of Gen Z and millennials say they aren’t comfortable at all when it comes to investing (29% and 27% respectively), and only 10% of our Gen Z & millennials say they are very comfortable with investments. To illustrate this point further, one-in-four of our respondents less than 38-years-old say that they “understand the importance of investing, but it’s too complicated.”

What Does This Mean for the Future of These Generations?

Gen Z is still coming of age and having to deal with money issues for the first time as they enter the workforce. For that reason, their concerns and priorities are more indicative of the here and now and maintaining the lifestyle that they want. As a generation focused on experiences over consuming, this makes sense. However, the fact that a third of this generation is already planning for retirement, outpacing the average American adult when it comes to saving, and showing a willingness to talk to others about their finances bodes well for their financial futures. This generation is also entering the best job market in years, which may also be a reason why they are more focused on things like travel and their lifestyle as they haven’t experience the economic strife that millennials did during the great recession.

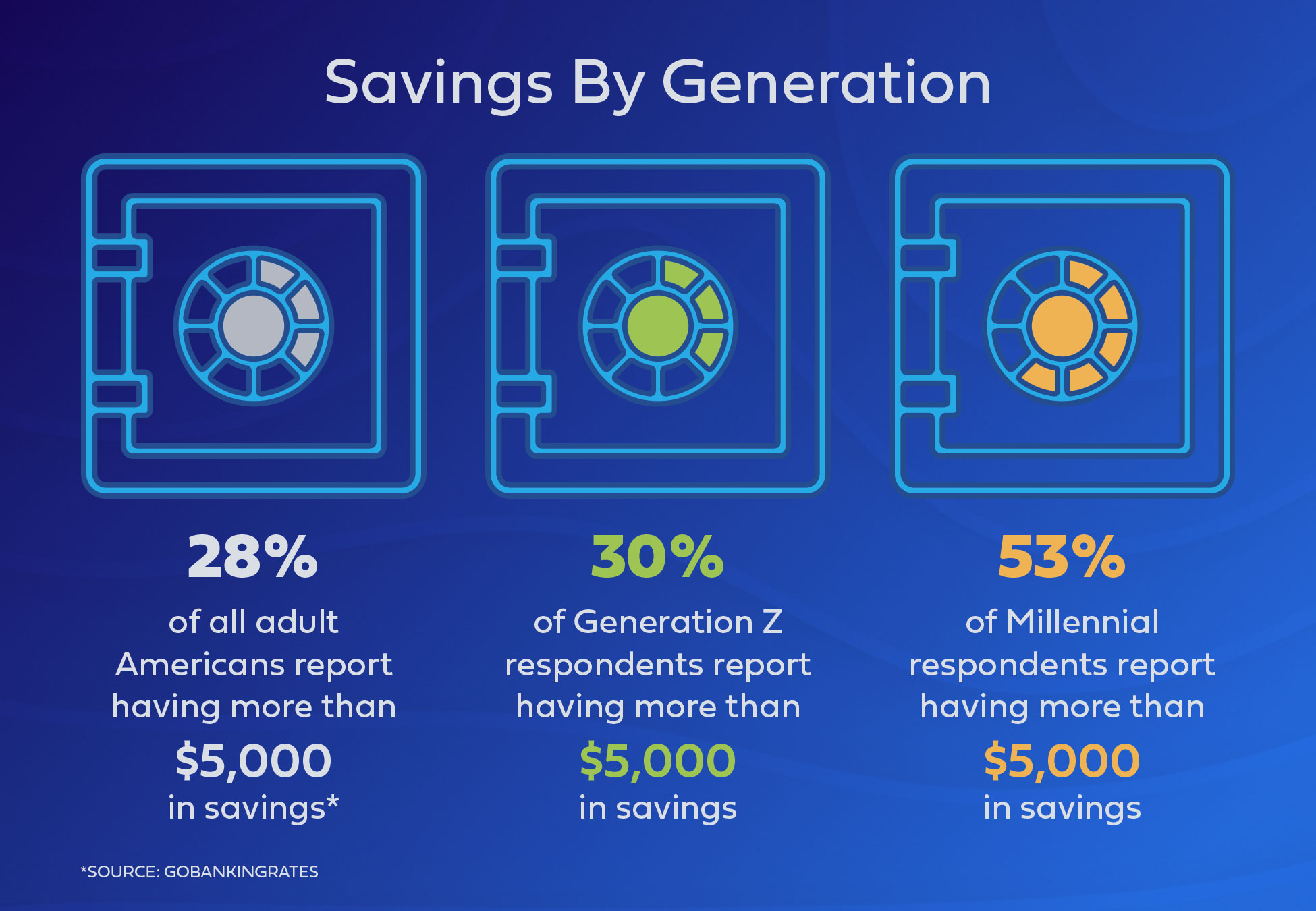

At first glance, it might appear that millennials are in a tough spot. However, their concern for paying their bills and building an emergency fund is likely a result of entering the workforce at the height of the Great Recession. However, despite a late start on building wealth, the scars from the recession have also instilled pragmatism. Millennials were more likely than Gen Z to say that the majority of their future wealth will be from a combination of salary and investments (35% vs. 32% respectively). Their apparent lower risk tolerance is also a welcomed sign. And while some may be a bit optimistic about retirement, recent studies show that nearly one-third of Americans 55-years-old and older don’t have any retirement nest egg. Our study also found that 53% of Millennials report having more than $5,000 in savings, compared to 28% of all Americans that report the same. So all in all, millennials are still doing better than the average American.

Perhaps the most important finding here is the fact that both generations simply don’t have the level of comfort with investing needed in order to take full advantage of it. While this begs for a reprioritization in a curriculum that focuses on financial literacy, the industry as a whole bears a responsibility to not only provide services, but also empower users to take full advantage of them through the proper education.

Gen Z and millennials are tech-savvy, practical generations that understand the importance of saving and investing. With their increasing expectations and spending power, they will play a massive role in shaping the future of the financial services industry. Fintechs and incumbent institutions alike would do well to understand their habits, concerns and views on money and apply them to their businesses. Those that do so now, will take leadership positions. Those that do not, will fall by the wayside.

Disclaimer

This information is educational, and is not an offer to sell or a solicitation of an offer to buy any security which can only be made through official documents such as a private placement memorandum or a prospectus. This information is not a recommendation to buy, hold, or sell an investment or financial product, or take any action. This information is neither individualized nor a research report, and must not serve as the basis for any investment decision. All investments involve risk, including the possible loss of capital. Past performance does not guarantee future results or returns. Neither Concreit nor any of its affiliates provides tax advice or investment recommendations and do not represent in any manner that the outcomes described herein or on the Site will result in any particular investment or tax consequence.Before making decisions with legal, tax, or accounting effects, you should consult appropriate professionals. Information is from sources deemed reliable on the date of publication, but Concreit does not guarantee its accuracy.

{kind=link}